Every day the financial media has stories about either impending doom or unbridled optimism for the stock market. Not surprisingly, many investors get the urge to move their asset allocations around based on these stories in the hopes of boosting their returns. They should resist that urge. While they might get lucky once and boost returns in the short term, they must get lucky twice to keep that excess return, or else they get financially hurt in the long run. So, do you feel lucky?

Market timing is the act of moving money in and out of the financial markets or switching between fund asset classes while trying to predict the future direction of the market. In other words, it involves making a series of decisions based on an endless cycle of fickle market and economic conditions.

Before giving in to the lure of market timing, here are some of the important factors to consider:

- Even if you sell your shares at the market’s peak, your good fortune is quickly on the line again when you try to guess the exact right time to re-enter the market. It requires two miracles to execute the perfect market timing trade – and then a third miracle if it can be repeated. Only Tom Cruise in Top Gun: Maverick has achieved three miracles.

- Market timing is a tedious, time-consuming, and imperfect pursuit that has no guarantee of success in the long run. Warren Buffett has said, “market timing is both impossible and stupid”.

- When you time the market, you’re betting against experienced market analysts who are also trying to make timely buying and selling decisions in an attempt to beat market averages. Yet even with all their experience and resources, those analysts and fund managers tend not to do much better than an index in the long run.

Of course, the financial media is designed to pander to emotional biases – otherwise, no one would read or watch any of the predictions they report on. It’s understandable that volatility in the market often tests the resolve of investors, and the more volatile the market the more likely investors will experience emotions like fear and even panic when it comes to their investments. But keep this in mind:

- Volatility is normal in an active market.

- If you’re a long-term investor, dozens of studies have shown that selling your stocks or funds during a volatile period may have a negative impact on your long-term returns.

- While it’s easy to get out of the market when things seem to be heading south, it’s also very easy to miss the best-performing days by not getting back in at just the right time. And if you miss those good days, your performance will likely be much worse than if you had simply stayed in the market the whole time.

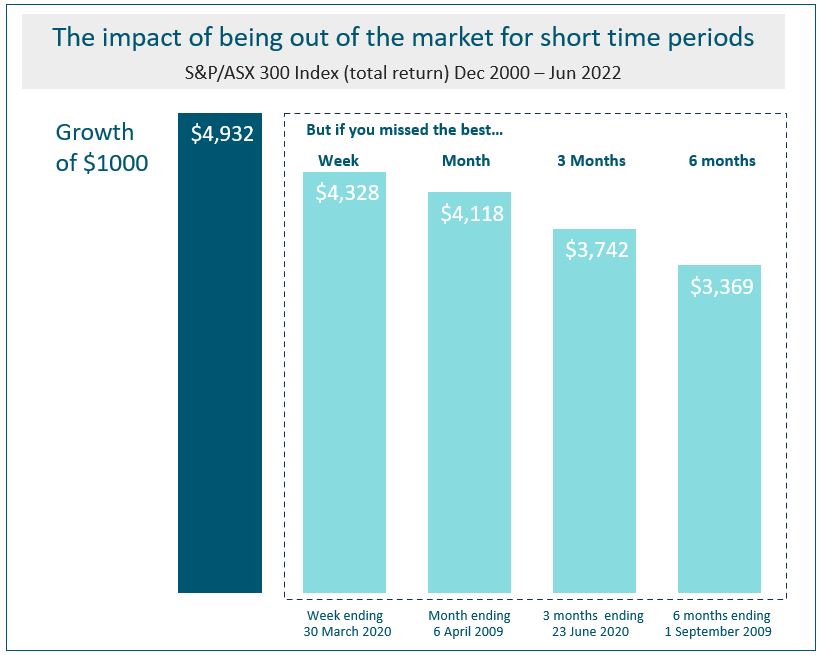

The impact of being out of the market for a short time can be profound, as shown by a hypothetical investment in the stocks that make up the S&P/ASX 300 Index.

In the example below, a hypothetical $1,000 investment made in 2000 turns into $4,932 for the 22-year period ending 30 June 2022. Over that 22-year period, it missed the S&P/ASX 300’s best week, which ended 30 March 2020, and the value shrunk to $4,328. Miss the best three months, which ended 23 June 2020, and the total return falls to $3,742.

Now the one major disclaimer that these sorts of charts never mention is that the opposite is also true – if you miss the worst week, worst month, etc then your returns are way better than just staying invested.

But how do you miss the worst periods without also risking missing the best periods? Staying invested and focused on the long term helps to ensure that you are in a position to capture what the market has to offer.

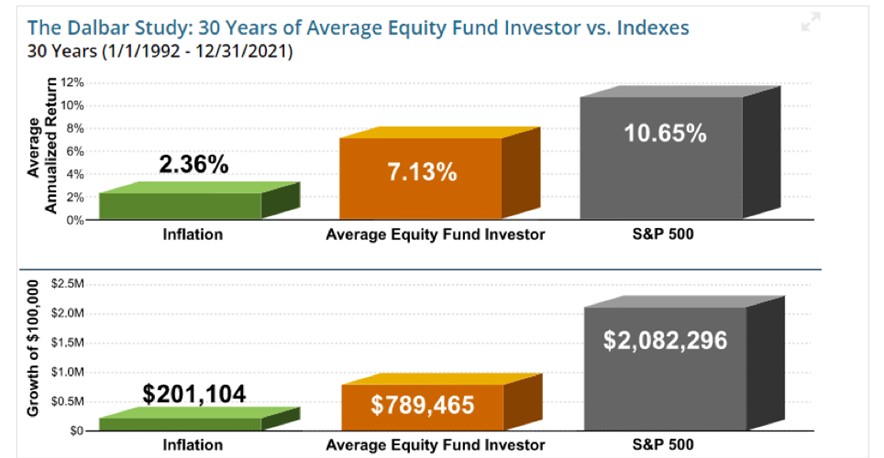

Another study from DALBAR entitled “Quantitative Analysis of Investor Behavior” shows the impact of market timing. This study out of the US shows that average investors consistently fail to achieve returns that are even close to matching the performance of broader market indices.

The chart below is from the 2022 study and shows how market timing behaviours in the US have contributed to performance. $100,000 invested 30 years ago would have grown to $2,082,296 had a US investor just left their money in the S&P 500 index. However, due to behavioural characteristics, the average equity fund investor missed out on nearly $1.3 million in value because their emotions took control and they tried to time the market.

There is plenty of evidence – both anecdotal and empirical – on why market timing just doesn’t work. It’s something that requires repeated miracles and plain old good luck to get it right. And to do it continuously requires a lot of miracles and a lot of luck.

A better approach is to always remember that stock market investing needs a long-term approach, and an ability to tune out the noise from the financial media. If you are considering moving your funds, move them strategically in a way that is consistent with the asset allocation that fits your long term investing objectives and risk tolerance.

https://www.nightviz.ca/single-post/top-gun-maverick-accomplishes-three-miracles

https://www.youtube.com/watch?v=secMNCDsxBc

https://www.spglobal.com/spdji/en/research-insights/spiva/#australia

Chart courtesy of Dimensional Fund Advisors. See https://my.dimensional.com/one-pagers/the-cost-of-trying-to-time-the-market for details on dates and disclaimers.

For information on Dalbar Inc and their QAIB report see https://www.ifa.com/articles/dalbar_2016_qaib_investors_still_their_worst_enemy

Source: Dalbar QAIB 2022 study, chart courtesy of Index Fund Advisors https://www.ifa.com

Dr Steve Garth PhD, M.App.Fin., BSc., BA. is the Principal of Principia Investment Consultants and works with Capital Partners assisting with communications.

For nearly two decades, Steve played a key role in helping grow the Australian arm of a global asset manager. During his career he managed Australian and global equity portfolios, managed the Asia Pacific trading team and for the last 10 years he managed the firm’s fixed interest strategies.

Steve received his PhD in Applied Mathematics from the Australian National University. He also holds a BSc in Mathematics and Physics, a BA with majors in History and Politics, a Master of Applied Finance.