The Reserve Bank of Australia (RBA) has taken another step in its gradual monetary easing cycle, cutting the official cash rate by 0.25 percentage points to 3.6%. The move, announced at the latest monetary policy meeting, reflects the central bank’s careful balancing act: keeping inflation under control while ensuring economic growth doesn’t stall.

At its most recent policy meeting on 13th August the RBA lowered the official cash rate from 3.85% to 3.6%. For households, businesses, and investors, this decision has direct implications—from mortgage repayments to business borrowing costs, to the broader confidence in Australia’s economy. Let’s unpack what happened, why it happened, and what could come next.

The RBA’s latest cut marks its second rate reduction this year, continuing a trend towards more accommodative policy. The official cash rate is now at 3.6%, down from 3.85% before the decision.

In its statement, the RBA emphasized two central points:

- Inflation is easing—though still elevated in some areas, it is moving closer to the target range.

- Global uncertainty remains high—international developments, especially in the US and China, could weigh on Australia’s growth prospects.

While the decision was widely anticipated by financial markets, its timing signals that the RBA is prioritizing sustained economic stability over aggressive tightening or loosening.

-

Inflation is easing

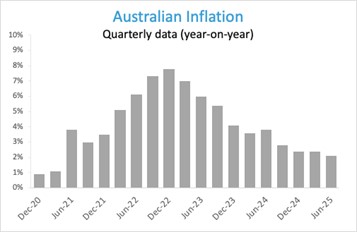

Inflation has been the central economic story of the past three years, surging in 2022 and early 2023 due to supply chain disruptions, strong consumer demand, and higher energy prices. However, recent data show that inflation is now moderating.

The RBA’s preferred measure, the trimmed mean inflation rate, came in at 2.1% in June, the lowest since 2021 and well within the 2–3% target band.

A slower pace of price increases eases pressure on household budgets and reduces the risk of inflation expectations becoming entrenched. This gives the RBA room to cut rates without immediately risking an inflation flare-up.

-

Global uncertainty

The international environment is still far from stable. The US faces ongoing trade tensions and possible economic slowdown, while China’s recovery has been uneven. Both economies have significant spillover effects on Australia, particularly through trade, investment, and commodity prices.

By easing rates now, the RBA is pre-emptively cushioning the economy against potential external shocks. It’s a classic “insurance” cut—acting before conditions worsen.

What’s happening in Australia’s economy?

As mentioned, inflation is easing but not evenly across sectors. Goods prices have stabilised, largely due to falling shipping costs and improved global supply chains. However, services inflation—especially in health, insurance, and education—remains stubbornly high.

For households, this means everyday expenses like groceries and petrol may feel more manageable, but other bills are still rising.

The unemployment rate rose slightly to 4.3%, indicating a softening labour market. While still historically low, this uptick suggests that hiring momentum is slowing. A modest increase in unemployment helps relieve wage-push inflation pressures but also raises concerns about consumer spending power.

Wages have been growing at their fastest pace in over a decade, driven by labour shortages in some industries and high living costs prompting demands for pay rises. While strong wage growth supports household income, it can also feed into business costs, which in turn may slow the pace of inflation’s decline.

Why the RBA is moving carefully

Central banking is a delicate balancing act between stimulating the economy and keeping inflation under control. The RBA doesn’t want to cut rates too quickly, which could reignite inflation, but it also wants to avoid keeping rates high for so long that the economy slows more than necessary.

By trimming rates by 0.25% rather than making a larger move, the RBA signals that it is taking a “wait and see” approach—responding to data rather than committing to an aggressive easing path.

What does this mean for interest rates going forward?

Market analysts broadly expect the RBA to continue with small, measured cuts through the rest of the year. If inflation continues to edge lower and the labour market doesn’t weaken too sharply, we could see the cash rate at around 3.35% by December.

However, the RBA has made it clear that its decisions will be data dependent. If inflation stalls above target or if wage growth accelerates further, rate cuts may pause—or even reverse.

How this affects you

Lower interest rates mean reduced borrowing costs for variable-rate loans. For a homeowner with a $600,000 mortgage, a 0.25% cut could mean savings of around $90–$100 a month, depending on the loan structure.

This extra breathing room can be significant for households still grappling with cost-of-living pressures. However, banks may not always pass on the full cut immediately, so it’s worth checking your lender’s policy.

Easing rates can make mortgages more affordable in the short term, but they can also boost housing demand, potentially putting upward pressure on prices. If you’re entering the market, it’s wise to focus on long-term affordability rather than just the initial monthly repayments.

On the flip side, lower rates reduce the return on savings accounts and term deposits. Retirees relying on interest income may need to seek alternative investments or adjust their budgets.

Cheaper borrowing costs can encourage businesses to invest in expansion, hire more staff, or upgrade equipment. However, uncertain demand and global risks may temper how aggressively companies act.

The broader economic impact

Rate cuts often boost consumer sentiment, making people feel more comfortable spending. Increased spending can help support retail, hospitality, and service sectors.

Equities tend to respond positively to lower interest rates, as they make shares more attractive relative to bonds and can improve corporate earnings prospects. Property markets may also see renewed interest from investors.

Lower rates can weaken the Australian dollar, making exports more competitive but increasing the cost of imports. This can help exporters but may keep imported goods prices higher.

Dr Steve Garth

August 2025

Dr Steve Garth PhD, M.App.Fin., BSc., BA. is the Principal of Principia Investment Consultants and works with Capital Partners assisting with communications.

For nearly two decades, Steve played a key role in helping grow the Australian arm of a global asset manager. During his career, he managed Australian and global equity portfolios, managed the Asia Pacific trading team and for the last 10 years he managed the firm’s fixed interest strategies.

Steve received his PhD in Applied Mathematics from the Australian National University. He also holds a BSc in Mathematics and Physics, a BA with majors in History and Politics, a Master of Applied Finance.