Treasurer Jim Chalmers delivered the 2026-27 Federal Budget last night. The package includes three major changes to tax which will force families to rethink how they structure their assets.

But first a cautionary note. The changes are not yet legislated, there is missing nuance we won’t get until further guidance is prepared, and – as always! – tax decisions shouldn’t drive investment decisions. It’s going to be a balancing act between setting yourself up in this new tax regime and not doing anything too early if there’s a risk it is unwound or revised.

- Capital Gains Tax Discount

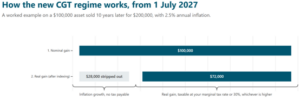

The Treasurer announced that from 1 July 2027, the current 50% CGT discount will be replaced by cost-base indexation and a minimum tax of 30%. Cost-base indexation would work something like:

- Cost base is indexed by CPI from the date of acquisition with the need to hold it for 12 months to receive indexation.

- You pay tax at the greater of 30% or your marginal tax rate on the indexed gain.

In this example, if your marginal tax rate was 47% your tax payable would be approximately $33,800, up from $23,500 under the old (though still current) regime.

Gains accrued before 1 July 2027 keep the 50% discount. Only gains after 1 July 2027 falls under the new rules. For our clients, the key question will likely be “should we sell before 1 July 2027?”

Ultimately this continues to be an investment decision and comes down to, do you want you want to sell the asset? Selling a good asset for tax is letting the tax tail wag the dog.

If you were planning to sell it around July 2027 anyway, there may be some niche cases where selling it before 30 June has a very marginal benefit, but this won’t be clear until we receive further technical guidance on how they will calculate tax on assets owned across the existing and proposed CGT regimes.

The biggest consideration going forward is where do you buy new investments given this change? As you can see in the example above, the shorter the hold period for an asset, the larger your taxable gain will be under the new regime. The holding structure, likely liquidation event (eg. gradual sell down vs all in one sale) and expected investment time horizon become important considerations.

What is likely to be important is maintaining excellent cost-base and valuation records, especially around 30 June / 1 July 2027. If you have unlisted assets, getting a valuation as at 1 July 2027 may be essential.

- Negative gearing

Negative gearing will be abolished for new residential property purchases, except for new residential property builds.

The change reportedly applies from 7:30pm on budget night (12 May 2026), with properties acquired before that time allowed to continue negative gearing until disposal (this includes contracts entered into but not settled).

From 1 July 2027, losses from established residential properties will only be deductible against rental income or residential-property capital gains, with excess losses carried forward.

Importantly, this change to negative gearing is only applicable to residential property – it does not extend to negative gearing in investment portfolios or commercial property. For the time being, those strategies can still be adopted.

Key considerations for our clients:

- If negative gearing through residential property was going to be part of your strategy in future, we need to reassess cash flow and borrowing capacity to determine whether this strategy is still right for you.

- Is negative gearing with an alternative asset class, like shares or commercial property, now more appropriate?

- As always, we need to consider whether any strategy you’ve adopted continues to be right for you, and going forward, if you have an existing negatively geared property, that may impact your decision to retain the property.

- Discretionary trusts

From 1 July 2028, trustees of discretionary trusts pay a minimum 30% tax on trust net income before any distribution to beneficiaries. Beneficiaries would receive non-refundable credits for tax paid by the trustee.

Corporate beneficiaries do not receive this tax credit, meaning income earned in a trust and distributed to a company attracts double taxation. This double taxation will receive lots of attention from industry, and the Government seems to be sending a clear message that corporate beneficiaries (or ‘bucket companies’) are not arrangements they want to see going forward.

The taxation of family trusts is the measure likely to have the most impact on our clients. Family trusts have been a common strategy for asset protection and flexible income distribution purposes for many years now, and while this measure will make them less attractive in many circumstances, the benefits they afford in asset protection, estate planning and income flexibility may remain compelling.

To assist small business’ who want to restructure, there is a three-year rollover relief window from 1 July 2027 to move assets from a discretionary trust to a company or fixed-unit trust. The detail on this rollover relief is not yet clear, and we note that stamp-duty is determined at a state level so how it’s treated needs to be clarified before any decisions can be made.

Key considerations in our advice process:

- It will be important to review family tax rates and trust distribution strategies before 1 July 2028, this will likely include modelling beneficiary tax outcomes under the proposed minimum-tax regime.

- Reassess whether trusts are still appropriate for your situation, keeping in mind that they still afford tax planning flexibility, asset protection and intergenerational wealth transfer benefits for the right circumstances.

- If a change is beneficial, how does the rollover relief apply to your situation, if at all, and what are the tax and stamp duty costs (if any) of changing structure.

- Companies as a structure may emerge as a more attractive long-term investment vehicle.

- Existing testamentary trusts have become even more valuable if that is one of your current structures. They retain the same benefits as they did before budget night, so there is a high level of flexibility.

- Lastly, we need to ensure that all your advisers are on the same page, we will continue to work closely with your accountant, estate-planning lawyer and any other professional advisers on your team to ensure we’re considering these changes across your entire situation.

What to do from here:

Every measure announced is government policy at this stage. Legislation has not yet been drafted or passed and none of the above has a hard and fast deadline to make decisions.

Some technical details (the CGT calculation method, the negative gearing transitional rule, and the precise scope of the trust rollover) will only become clear when exposure draft legislation is released. We will write again as those details emerge and discuss them with you at your upcoming client meetings.

If you have any questions in the meantime, please contact your adviser.