In mid-2024, every major currency in the world had fallen against the US dollar, an unusually broad shift with significant consequences for the global economy. The strength of the greenback (US dollar) stemmed from a shift in expectations about when and by how much the Federal Reserve would cut its benchmark interest rate, which was then at a 20-year high. The episode is a useful case study in how interest rate differentials between countries drive currency movements, and in how quickly that dynamic can shift.

Why the US Dollar Was So Strong

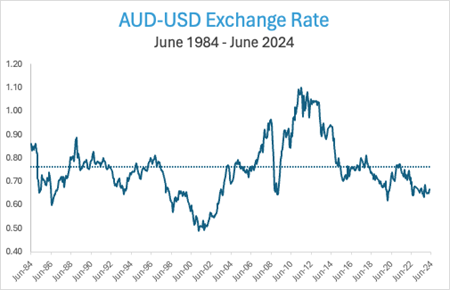

High US interest rates, a response to stubborn inflation, had propelled the dollar to an unusually high level against other major currencies. The US dollar index, a common measure of the US currency’s strength against a basket of its major trading partners, was hovering at levels last seen in the early 2000s. For instance, the Australian dollar had been trading around 66 cents, below its 40-year average of 75 cents, for the prior two years, while the Chinese yuan showed notable signs of weakness despite officials’ efforts to stabilise it.

The dollar’s dominance in global trade is profound: it sits on one side of nearly 90 per cent of all foreign exchange transactions. A stronger US currency intensifies inflation abroad, as countries need to exchange more of their own currency for the same amount of dollar-denominated goods, including essential commodities like oil. Countries with dollar-denominated debt also face higher interest payments, compounding their financial pressures.

Interest rate differentials are the core mechanism at work here: higher rates attract more foreign capital, strengthening a country’s currency relative to others. The spike in inflation after the pandemic forced central banks worldwide to raise interest rates aggressively to bring it under control. By mid-2024, after more than two years of the fastest interest rate tightening cycle in decades, the US had one of the highest interest rates in the developed world, with a target range of 5.25 to 5.50 per cent. Australia’s cash rate, by comparison, had sat at a more modest 4.35 per cent since November 2023.

What Markets Expected, and What Actually Happened

Markets had been expecting US interest rates to start falling, and the US dollar to weaken, since late 2023. The Federal Reserve had signalled no further rate increases were planned, and that the next move would be a cut. However, persistently high prices forced the Federal Reserve to hold rates higher for longer than expected, keeping the US dollar stronger for an extended period.

This left policymakers around the world balancing a difficult choice: support their domestic economy by cutting interest rates, or support their currency by keeping rates high. The longer a country held rates high to defend its currency, the more its domestic economy risked suffering as a result.

Global Pressures and Local Realities

China’s situation illustrated this tension clearly. A real estate crisis and sluggish domestic spending had battered its economy, and China ultimately relaxed its stance and allowed the yuan to weaken, demonstrating the pressure a strong US dollar placed on financial markets and policy decisions worldwide.

Interest rate differentials significantly influence exchange rates, but they are not the only factor. In Australia’s case, the dollar is also influenced by commodity prices, the strength of its largest trading partner, China, and other global conditions. Many investors had expected the US to begin cutting rates before Australia did, which would have narrowed the rate differential and strengthened the Australian dollar. Instead, stubborn inflation kept rates on hold in both countries for longer than expected, leaving those investors caught off guard. Some commentators at the time believed the AUD would return to its long-term average of 75 cents, though there was no certainty about whether, or when, that would happen.

What’s Changed Since

Why is the US dollar so strong at any given point, and does it stay that way? Not necessarily. The mechanism described above has since moved in the other direction. The Federal Reserve has cut its benchmark rate substantially since mid-2024, bringing the target range down to 3.50 to 3.75 per cent, while the RBA’s cash rate sits at 4.35 per cent. With the US-Australia rate gap now far narrower than it was in 2024, the Australian dollar has recovered accordingly, trading closer to 69 to 70 US cents.

This is exactly the pattern the interest rate differential model would predict: as the gap between two countries’ interest rates narrows, the currency of the higher-rate country tends to strengthen. The broader lesson holds regardless of which direction the dollar happens to be moving in any given year: currency markets respond to relative, not absolute, conditions, and today’s dominant trend is rarely a reliable guide to next year’s.

What This Means for Your Portfolio

Currency movements like these are a reminder of why a genuinely diversified investment strategy matters, rather than a portfolio concentrated in any single currency, market, or asset class. Our evidence-based investment philosophy is built around managing these kinds of macro shifts through structure and diversification, rather than trying to predict them.

If you’d like to talk through how currency and interest rate movements affect your own portfolio, get in touch with our team.

Dr Steve Garth June 2024

Dr Steve Garth PhD, M.App.Fin., BSc., BA. is the Principal of Principia Investment Consultants and works with Capital Partners assisting with communications.

For nearly two decades, Steve played a key role in helping grow the Australian arm of a global asset manager. During his career, he managed Australian and global equity portfolios, managed the Asia Pacific trading team, and for the last 10 years managed the firm’s fixed interest strategies.

Steve received his PhD in Applied Mathematics from the Australian National University. He also holds a BSc in Mathematics and Physics, a BA with majors in History and Politics, and a Master of Applied Finance.