Financial markets are in a period of uncertainty. Central bankers are unsure whether they’ve done enough – or not enough – to get inflation back to their 2 to 3 percent target band. Economists and market commentators have now danced from the “hard landing” scenario which seemed certain earlier in the year to the “soft landing” scenario in July and are now waltzing into the “could be hard or could be soft” scenario. Without any clear guidance, markets are just dancing in the dark…

Back at the end of August Fed Chair Jerome Powell concluded his speech at the annual Jackson Hole conference of central bankers, economists, and other policymakers that the US Federal Reserve Board was “navigating by the stars under cloudy skies”.

This admission of the uncertainties inherent in monetary policy sums up the mood of financial markets. Central bankers are unsure whether they’ve done enough to move inflation rates on a path towards their desired targets of around 2 to 3 percent. Bond yields continue to inch higher, indicating that there is every chance another rate hike is in store.

But for most of the year equities have ignored the 12 interest rate rises that the RBA has handed out since May last year. By the end of July, the Australian market had reached a respectable year-to-date return of 8% – despite a serious wobble in March as stress in the US banking system had ramifications around the world.

But as the chart below shows since the end of July the market has lost traction and is now giving up those gains. As we approach the end of October the ASX 200 index is up a meager 1.5% year to date.

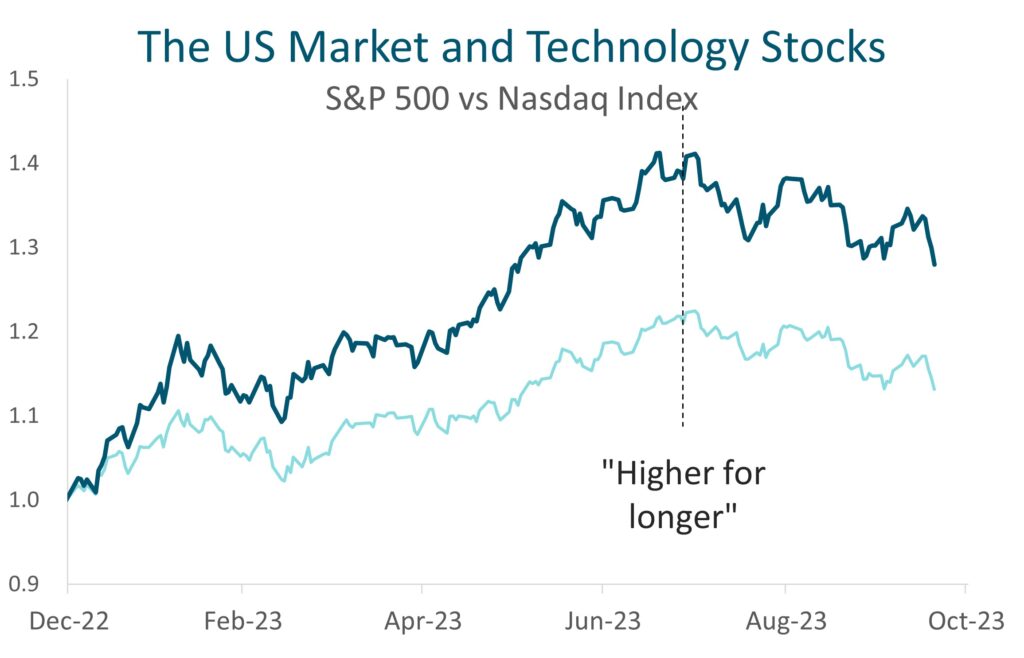

By the end of July, the US market (represented by the S&P 500 Index) was up 22% (in US dollar terms). Much of that performance was driven by the “magnificent 7” big tech stocks, which had propelled the Nasdaq composite index (which makes up about 45% of the US market) to a staggering 39% year to date. But by the end of October, the US market was in correction territory, having fallen by more than 10% since the peak.

What has brought about the end of the stock market rally? One explanation is that equity markets finally realized that central banks were serious when they kept reiterating that they now see interest rates staying “higher for longer”.

Much of the support for equities over the year has been driven by the equity market’s belief that the ‘terminal rate’ for this cycle of interest rates was close and that central banks would start cutting rates as soon as the end of this year. Contributing to this narrative was the data showing inflation continued to decline and a better-than-expected earnings season.

However, the market mood is souring as officials continue to signal that rates will not be coming down anytime soon. Middle East tension and surging US bond yields have set up financial markets for more turbulence in the coming weeks, exacerbated by high oil prices and China’s property pain.

In the near term, what central banks do as they enter the final phase of this fight with inflation will have a big impact on the value of stocks, bonds, and currencies and, of course, on the broader economy. With no clear indication on whether a recession is still on the cards, global stock markets are now dancing in the dark.

With this market and economic uncertainty, investors may be tempted to abandon equities as there is a heightened risk of a recession. But stock prices incorporate these expectations and generally fall in value before a recession even begins. And given that stocks are off their July highs we may be witnessing nothing more than a typical correction before the start of the next rally. As always, Investors who look beyond headlines about markets and the economy and stick to a plan will be better positioned for long-term success.

Dr Steve Garth PhD, M.App.Fin., BSc., BA. is the Principal of Principia Investment Consultants and works with Capital Partners assisting with communications.

For nearly two decades, Steve played a key role in helping grow the Australian arm of a global asset manager. During his career, he managed Australian and global equity portfolios, managed the Asia Pacific trading team and for the last 10 years he managed the firm’s fixed interest strategies.

Steve received his PhD in Applied Mathematics from the Australian National University. He also holds a BSc in Mathematics and Physics, a BA with majors in History and Politics, a Master of Applied Finance.